Super.money, the financial service platform that Walmart’s Flipkart launched last year, has quietly entered a partnership with payments infrastructure company Juspay. This collaboration supports Super.money’s expansion into direct-to-consumer (D2C) checkout services, with the goal of reaching $100 million in annual revenue by 2026.

This partnership arises as Juspay aims to regain its footing after experiencing resistance from major payment firms earlier this year, a situation that made its fundraising more challenging.

Super.money recently introduced its D2C checkout solution, Super.money Breeze, which promises retailers a streamlined, one-click checkout process. This product is designed to accelerate online shopping by eliminating the need for one-time passwords and repeated logins. While Super.money has not publicly named its technology partners, TechCrunch has discovered that Juspay is providing the payments infrastructure for this new offering.

This initiative could help Super.money attract a wider range of customers and increase its visibility among D2C brands, extending its market reach beyond Flipkart’s existing user base and boosting brand recognition among online consumers. Although Super.money already benefits from Flipkart’s distribution network, the new checkout product indicates a push to establish an independent brand within the broader e-commerce landscape.

For Juspay, this partnership holds even greater significance as it seeks to rebuild its relationships with Indian merchants. The SoftBank-backed company experienced losses when payment gateways like Razorpay and Cashfree Payments began moving away from Juspay in January, encouraging merchants to use their own internal payment processing tools instead. This shift affected Juspay’s fundraising efforts, with the most recent round totaling $60 million, less than the initially anticipated $100 million, according to TechCrunch sources.

Juspay was once a favored back-end partner for payment aggregators, helping them minimize transaction failures through its payment routing platform. Amazon is among its long-standing clients, and Juspay received a payment aggregator license from the Reserve Bank of India last year. However, as competition intensifies within India’s digital payments sector, companies such as Razorpay, Cashfree, and Flipkart spinoff PhonePe have started to reduce their reliance on external providers, choosing instead to strengthen their direct connections with merchants.

Super.money’s decision to team up with Juspay contrasts with the prevailing trend of payment companies developing and managing their own infrastructure. However, for a young fintech company still broadening its scope beyond Flipkart, this partnership offers a quick path to D2C integrations without needing to create comprehensive payment capabilities from scratch. It also demonstrates Super.money’s aim to engage more deeply in consumer transactions and increase payment volumes through its platform.

Techcrunch event

San Francisco

|

October 27-29, 2025

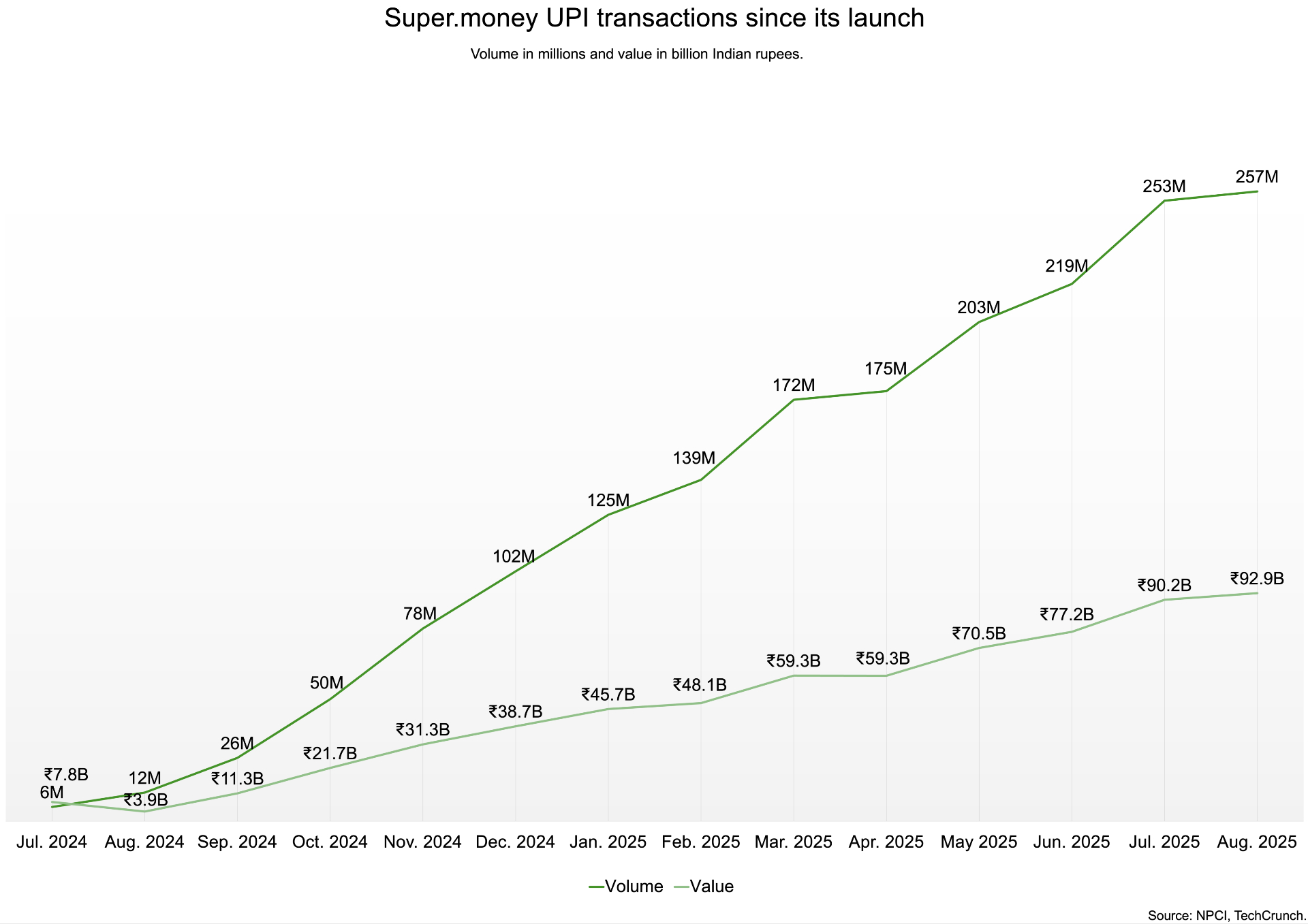

Since launching as a payment app in June 2024, more than a year after Flipkart’s formal separation from PhonePe, Super.money has risen to become one of India’s top five UPI (Unified Payments Interface) apps in terms of transaction volume. UPI is India’s government-supported real-time payment system. According to data from the National Payments Corporation of India, the organization overseeing the UPI system, Super.money processed over 200 million transactions monthly for four consecutive months through August.

In recent months, Super.money has overtaken major private banks, including Axis Bank and ICICI Bank, as well as fintech companies like Amazon Pay and CRED, to improve its position in the UPI rankings — a notable achievement for a recently established app.

Super.money has also risen to be a leading issuer of secured credit cards in India, capturing 10% of the market share, as per industry data shared with TechCrunch by an informed source. These cards require customers to provide a security deposit and are currently offered in partnership with Utkarsh Small Finance Bank. The company is planning to grow this segment and is discussing collaboration with a private sector lender to broaden its distribution, according to a source familiar with the matter.

To date, Super.money has issued roughly 300,000 secured cards and is adding about 50,000 new cards each month, the source added.

The secured card business is a key component of Super.money’s monetization approach, enabling it to transition users from low-margin UPI payments to more profitable financial products. While UPI transactions are free, Super.money leverages this volume to attract customers and promote higher-yield products, such as credit cards and consumer loans.

Unlike many other fintechs focused on UPI, Super.money has managed to keep its expenditure low by utilizing Flipkart’s distribution network instead of investing heavily in marketing. TechCrunch has learned that the company also maintains a small team of approximately 130 to 150 employees to serve its user base of over 80 million.

For Flipkart, Super.money signifies a renewed commitment to fintech following the formal spin-off of PhonePe in 2023. While PhonePe has since dominated India’s UPI sector, it now functions independently within Walmart’s larger corporate structure. In contrast, Super.money remains closely connected with Flipkart and is apparently focused on monetizing financial services directly within — and beyond — the e-commerce ecosystem.

Flipkart has initially invested $50 million in Super.money to launch its operations. The business is headed by Prakash Sikaria, previously Flipkart’s chief experience officer for customer growth, marketing, advertising, and new ventures, and also the founder of Shopsy. According to his LinkedIn profile, Sikaria also played a role in Flipkart’s acquisition of the online travel agency Cleartrip and oversaw products like Flipkart Ads and SuperCoins.

However, Super.money intends to expand beyond Flipkart and seek external funding. Sources have informed TechCrunch that the company is already in discussions with bankers and plans to raise capital at a valuation of around $1 billion sometime next year.

TechCrunch has learned that Super.money is on track to conclude 2025 with about $30 million in annual recurring revenue. The company aims to increase this figure more than threefold in 2026, primarily through growth in its secured credit card business and personal lending, along with initiatives like the recently launched D2C checkout product.

That being said, Super.money is currently in the early stages of monetization and will likely face increasing competition from established players such as PhonePe, Google Pay, and Razorpay — all of which are either building or reinforcing their own payments infrastructure. Its success in converting UPI scale into lasting revenue, especially through lending and checkout infrastructure, will determine whether it can become Flipkart’s next major fintech success or encounter the same ecosystem challenges currently affecting its partner, Juspay.

Flipkart, Sikaria, and Juspay co-founder and CEO Vimal Kumar have not yet responded to requests for comments.